Essential Tools: Pandas#

Pandas is the Python Data Analysis Library.

Pandas is an extremely versatile tool for manipulating datasets.

It also produces high quality plots with matplotlib, and integrates nicely with other libraries that expect NumPy arrays.

Use of Pandas is a data science best practice.

The most important tool provided by Pandas is the data frame.

A data frame is a table in which each row and column is given a label.

Pandas DataFrames are documented at:

http://pandas.pydata.org/pandas-docs/dev/generated/pandas.DataFrame.html

Get in the habit: whenever you load data, place it into a dataframe as your first step.

Getting started#

import pandas as pd

import pandas_datareader.data as web

from pandas import Series, DataFrame

import matplotlib.pyplot as plt

import seaborn as sns

from datetime import datetime

#pd.__version__

%matplotlib inline

Fetching, storing and retrieving your data#

For demonstration purposes, we’ll use a utility library that fetches data from standard online sources, such as Yahoo! Finance.

import yfinance as yf

yahoo_stocks = pd.DataFrame(yf.download('YELP',start='2015-01-01',end='2015-12-31', progress = False))

yahoo_stocks.head()

| Open | High | Low | Close | Adj Close | Volume | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 |

This is a typical example of a dataframe.

Notice how each row has a label and each column has a label.

A dataframe is an object that has many methods associated with it, to do all sorts of useful things.

Here is a simple method: .info()

yahoo_stocks.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 251 entries, 2015-01-02 to 2015-12-30

Data columns (total 6 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Open 251 non-null float64

1 High 251 non-null float64

2 Low 251 non-null float64

3 Close 251 non-null float64

4 Adj Close 251 non-null float64

5 Volume 251 non-null int64

dtypes: float64(5), int64(1)

memory usage: 13.7 KB

Reading to/from a .csv file#

Continuing to explore methods, let’s write the dataframe out to a .csv file:

yahoo_stocks.to_csv('yahoo_data.csv')

!head yahoo_data.csv

Date,Open,High,Low,Close,Adj Close,Volume

2015-01-02,55.459999084472656,55.599998474121094,54.2400016784668,55.150001525878906,55.150001525878906,1664500

2015-01-05,54.540000915527344,54.95000076293945,52.33000183105469,52.529998779296875,52.529998779296875,2023000

2015-01-06,52.54999923706055,53.93000030517578,50.75,52.439998626708984,52.439998626708984,3762800

2015-01-07,53.31999969482422,53.75,51.7599983215332,52.209999084472656,52.209999084472656,1548200

2015-01-08,52.59000015258789,54.13999938964844,51.7599983215332,53.83000183105469,53.83000183105469,2015300

2015-01-09,55.959999084472656,56.9900016784668,54.720001220703125,56.06999969482422,56.06999969482422,6224200

2015-01-12,56.0,56.060001373291016,53.43000030517578,54.02000045776367,54.02000045776367,2407700

2015-01-13,54.470001220703125,54.79999923706055,52.52000045776367,53.18000030517578,53.18000030517578,1958400

2015-01-14,52.79999923706055,53.68000030517578,51.459999084472656,52.20000076293945,52.20000076293945,1854600

And of course we can likewise read a .csv file into a dataframe. This is probably the most common way you will get data into Pandas.

df = pd.read_csv('yahoo_data.csv')

df.head()

| Date | Open | High | Low | Close | Adj Close | Volume | |

|---|---|---|---|---|---|---|---|

| 0 | 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 |

| 1 | 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 |

| 2 | 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 |

| 3 | 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 |

| 4 | 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 |

Working with data columns#

In general, we’ll usually organize things so that rows in the dataframe are items and columns are features.

df.columns

Index(['Date', 'Open', 'High', 'Low', 'Close', 'Adj Close', 'Volume'], dtype='object')

Pandas allows you to use standard python indexing to refer to columns (eg features) in your dataframe:

df['Open']

0 55.459999

1 54.540001

2 52.549999

3 53.320000

4 52.590000

...

246 27.950001

247 28.270000

248 28.120001

249 27.950001

250 28.580000

Name: Open, Length: 251, dtype: float64

Pandas also allows you to use a syntax like an object attribute to refer to a column.

But note that the column name cannot include a space in this case.

df.Open

0 55.459999

1 54.540001

2 52.549999

3 53.320000

4 52.590000

...

246 27.950001

247 28.270000

248 28.120001

249 27.950001

250 28.580000

Name: Open, Length: 251, dtype: float64

You can select a list of columns:

df[['Open','Close']].head()

| Open | Close | |

|---|---|---|

| 0 | 55.459999 | 55.150002 |

| 1 | 54.540001 | 52.529999 |

| 2 | 52.549999 | 52.439999 |

| 3 | 53.320000 | 52.209999 |

| 4 | 52.590000 | 53.830002 |

Putting things together – make sure this syntax is clear to you:

df.Date.head(10)

0 2015-01-02

1 2015-01-05

2 2015-01-06

3 2015-01-07

4 2015-01-08

5 2015-01-09

6 2015-01-12

7 2015-01-13

8 2015-01-14

9 2015-01-15

Name: Date, dtype: object

df.Date.tail(10)

241 2015-12-16

242 2015-12-17

243 2015-12-18

244 2015-12-21

245 2015-12-22

246 2015-12-23

247 2015-12-24

248 2015-12-28

249 2015-12-29

250 2015-12-30

Name: Date, dtype: object

Changing column names is as simple as assigning to the .columns property.

Let’s adjust column names so that none of them include spaces:

new_column_names = [x.lower().replace(' ','_') for x in df.columns]

df.columns = new_column_names

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 251 entries, 0 to 250

Data columns (total 7 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 251 non-null object

1 open 251 non-null float64

2 high 251 non-null float64

3 low 251 non-null float64

4 close 251 non-null float64

5 adj_close 251 non-null float64

6 volume 251 non-null int64

dtypes: float64(5), int64(1), object(1)

memory usage: 13.9+ KB

(Be sure you understand the list comprehension used above – it’s a common and important way to process a list in python.)

Now all columns can be accessed using the dot notation:

df.adj_close.head()

0 55.150002

1 52.529999

2 52.439999

3 52.209999

4 53.830002

Name: adj_close, dtype: float64

A sampling of DataFrame methods.#

A dataframe object has many useful methods.

Familiarize yourself with dataframe methods – they are very useful.

These should be self-explanatory.

df[['high', 'low', 'open', 'close', 'volume', 'adj_close']].mean()

high 3.809084e+01

low 3.659777e+01

open 3.732426e+01

close 3.733303e+01

volume 3.501135e+06

adj_close 3.733303e+01

dtype: float64

df[['high', 'low', 'open', 'close', 'volume', 'adj_close']].std()

high 1.138931e+01

low 1.114006e+01

open 1.128846e+01

close 1.126194e+01

volume 4.152341e+06

adj_close 1.126194e+01

dtype: float64

df[['high', 'low', 'open', 'close', 'volume', 'adj_close']].median()

high 3.909000e+01

low 3.665000e+01

open 3.822000e+01

close 3.818000e+01

volume 2.356000e+06

adj_close 3.818000e+01

dtype: float64

df.open.mean()

37.3242629229785

df.high.mean()

38.09083672633684

Plotting methods#

Pandas has an extensive library of plotting functions, and they are very easy to use.

These are your “first look” functions.

(Later you will use specialized graphics packages for more sophisticated visualizations.)

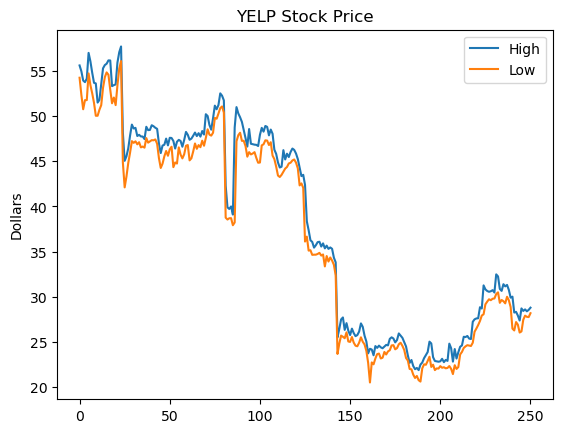

df.high.plot(label='High')

df.low.plot(label='Low')

plt.title('YELP Stock Price')

plt.ylabel('Dollars')

plt.legend(loc='best');

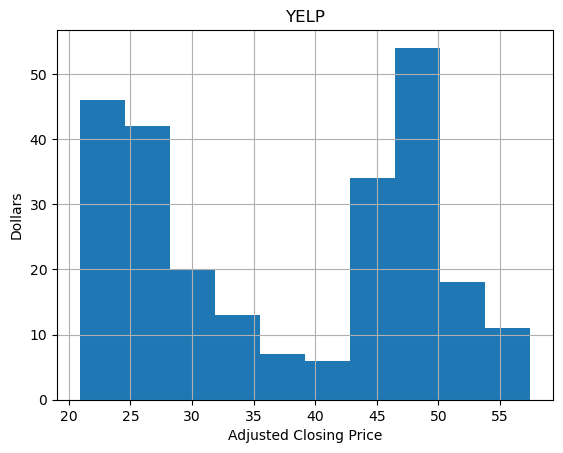

df.adj_close.hist()

plt.xlabel('Adjusted Closing Price')

plt.ylabel('Dollars')

plt.title('YELP');

Bulk Operations#

Methods like sum() and std() work on entire columns.

We can run our own functions across all values in a column (or row) using apply().

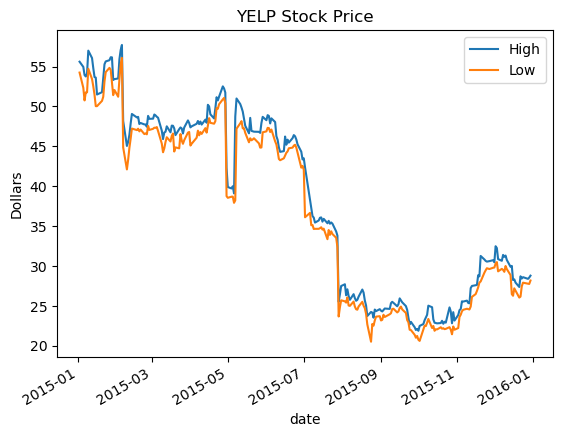

As an example, let’s go back to this plot:

df.high.plot(label='High')

df.low.plot(label='Low')

plt.title('YELP Stock Price')

plt.ylabel('Dollars')

plt.legend(loc='best');

It’s almost perfect. The only problem is the \(x\)-axis: it should show time.

To fix this, we need to make the dataframe index – that is, the row labels – into dates.

We have a problem however: the “dates” in our data are only strings. We need Pandas to understand that they are actually dates.

df.date.head()

0 2015-01-02

1 2015-01-05

2 2015-01-06

3 2015-01-07

4 2015-01-08

Name: date, dtype: object

The values property of the column returns a list of values for the column. Inspecting the first value reveals that these are strings with a particular format.

first_date = df.date.values[0]

first_date

'2015-01-02'

To convert these strings to actual dates we’ll use the datetime standard python package:

datetime.strptime(first_date, "%Y-%m-%d")

datetime.datetime(2015, 1, 2, 0, 0)

And to do this for each string in the date column we will use .apply():

new_df = df.copy()

new_df.date = df.date.apply(lambda d: datetime.strptime(d, "%Y-%m-%d"))

new_df.date.head()

0 2015-01-02

1 2015-01-05

2 2015-01-06

3 2015-01-07

4 2015-01-08

Name: date, dtype: datetime64[ns]

Each row in a DataFrame is associated with an index, which is a label that uniquely identifies a row.

The row indices so far have been auto-generated by pandas, and are simply integers starting from 0.

Fixing this is as easy as assigning to the index property of the DataFrame.

new_df.index = new_df.date

new_df.head()

| date | open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|---|

| date | |||||||

| 2015-01-02 | 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 |

| 2015-01-05 | 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 |

| 2015-01-06 | 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 |

| 2015-01-07 | 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 |

| 2015-01-08 | 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 |

Now that we have made an index based on a real date, we can drop the original date column.

new_df = new_df.drop(['date'],axis=1)

new_df.head()

| open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 |

Now we can see that Pandas handles these dates quite nicely:

new_df.high.plot(label='High')

new_df.low.plot(label='Low')

plt.title('YELP Stock Price')

plt.ylabel('Dollars')

plt.legend(loc='best');

Accessing rows of the DataFrame#

So far we’ve seen how to access a column of the DataFrame. To access a row we use a different notation.

To access a row by its index value, use the .loc() method.

new_df.loc[datetime(2015,1,23,0,0)]

open 5.466000e+01

high 5.564000e+01

low 5.430000e+01

close 5.519000e+01

adj_close 5.519000e+01

volume 1.636400e+06

Name: 2015-01-23 00:00:00, dtype: float64

To access a row by its sequence number (ie, like an array index), use .iloc() (‘Integer Location’)

new_df.iloc[0,:]

open 5.546000e+01

high 5.560000e+01

low 5.424000e+01

close 5.515000e+01

adj_close 5.515000e+01

volume 1.664500e+06

Name: 2015-01-02 00:00:00, dtype: float64

To iterate over the rows, use .iterrows()

num_positive_days = 0

for idx, row in df.iterrows():

if row.close > row.open:

num_positive_days += 1

print("The total number of positive-gain days is {}.".format(num_positive_days))

The total number of positive-gain days is 125.

Filtering#

It is easy to select interesting rows from the data.

All the operations below return a new DataFrame, which itself can be treated the same way as all DataFrames we have seen so far.

tmp_high = new_df.high > 55

tmp_high.head()

date

2015-01-02 True

2015-01-05 False

2015-01-06 False

2015-01-07 False

2015-01-08 False

Name: high, dtype: bool

Summing a Boolean array is the same as counting the number of True values.

sum(tmp_high)

11

Now, let’s select only the rows of df1 that correspond to tmp_high

new_df[tmp_high]

| open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 |

| 2015-01-09 | 55.959999 | 56.990002 | 54.720001 | 56.070000 | 56.070000 | 6224200 |

| 2015-01-12 | 56.000000 | 56.060001 | 53.430000 | 54.020000 | 54.020000 | 2407700 |

| 2015-01-22 | 53.869999 | 55.279999 | 53.119999 | 54.799999 | 54.799999 | 2295400 |

| 2015-01-23 | 54.660000 | 55.639999 | 54.299999 | 55.189999 | 55.189999 | 1636400 |

| 2015-01-26 | 55.119999 | 55.790001 | 54.830002 | 55.410000 | 55.410000 | 1450300 |

| 2015-01-27 | 56.060001 | 56.160000 | 54.570000 | 55.630001 | 55.630001 | 2410400 |

| 2015-01-28 | 56.150002 | 56.150002 | 52.919998 | 53.000000 | 53.000000 | 2013100 |

| 2015-02-03 | 53.830002 | 55.930000 | 53.410000 | 55.779999 | 55.779999 | 2885400 |

| 2015-02-04 | 55.529999 | 57.070000 | 55.250000 | 56.740002 | 56.740002 | 2498600 |

| 2015-02-05 | 57.599998 | 57.700001 | 56.080002 | 57.470001 | 57.470001 | 4657300 |

Putting it all together, we have the following commonly-used patterns:

positive_days = new_df[new_df.close > new_df.open]

positive_days.head()

| open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 |

| 2015-01-09 | 55.959999 | 56.990002 | 54.720001 | 56.070000 | 56.070000 | 6224200 |

| 2015-01-16 | 50.180000 | 51.490002 | 50.029999 | 51.389999 | 51.389999 | 2183300 |

| 2015-01-21 | 51.200001 | 53.500000 | 51.200001 | 53.410000 | 53.410000 | 3248100 |

| 2015-01-22 | 53.869999 | 55.279999 | 53.119999 | 54.799999 | 54.799999 | 2295400 |

very_positive_days = new_df[(new_df.close - new_df.open) > 4]

very_positive_days.head()

| open | high | low | close | adj_close | volume | |

|---|---|---|---|---|---|---|

| date | ||||||

| 2015-05-07 | 38.220001 | 48.73 | 38.220001 | 47.009998 | 47.009998 | 33831600 |

Creating new columns#

To create a new column, simply assign values to it. Think of the columns as a dictionary:

new_df['profit'] = (new_df.open < new_df.close)

new_df.head()

| open | high | low | close | adj_close | volume | profit | |

|---|---|---|---|---|---|---|---|

| date | |||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 | False |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 | False |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 | False |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 | False |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 | True |

Let’s give each row a gain value as a categorical variable:

for idx, row in new_df.iterrows():

if row.open > row.close:

new_df.loc[idx,'gain']='negative'

elif (row.close - row.open) < 1:

new_df.loc[idx,'gain']='small_gain'

elif (row.close - row.open) < 6:

new_df.loc[idx,'gain']='medium_gain'

else:

new_df.loc[idx,'gain']='large_gain'

new_df.head()

| open | high | low | close | adj_close | volume | profit | gain | |

|---|---|---|---|---|---|---|---|---|

| date | ||||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 | False | negative |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 | False | negative |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 | False | negative |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 | False | negative |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 | True | medium_gain |

Here is another, more “functional”, way to accomplish the same thing.

Define a function that classifies rows, and apply it to each row.

def namerow(row):

if row.open > row.close:

return 'negative'

elif (row.close - row.open) < 1:

return 'small_gain'

elif (row.close - row.open) < 6:

return 'medium_gain'

else:

return 'large_gain'

new_df['test_column'] = new_df.apply(namerow, axis = 1)

new_df.head()

| open | high | low | close | adj_close | volume | profit | gain | test_column | |

|---|---|---|---|---|---|---|---|---|---|

| date | |||||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 | False | negative | negative |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 | False | negative | negative |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 | False | negative | negative |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 | False | negative | negative |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 | True | medium_gain | medium_gain |

OK, point made, let’s get rid of that extraneous test_column:

new_df.drop('test_column', axis = 1)

| open | high | low | close | adj_close | volume | profit | gain | |

|---|---|---|---|---|---|---|---|---|

| date | ||||||||

| 2015-01-02 | 55.459999 | 55.599998 | 54.240002 | 55.150002 | 55.150002 | 1664500 | False | negative |

| 2015-01-05 | 54.540001 | 54.950001 | 52.330002 | 52.529999 | 52.529999 | 2023000 | False | negative |

| 2015-01-06 | 52.549999 | 53.930000 | 50.750000 | 52.439999 | 52.439999 | 3762800 | False | negative |

| 2015-01-07 | 53.320000 | 53.750000 | 51.759998 | 52.209999 | 52.209999 | 1548200 | False | negative |

| 2015-01-08 | 52.590000 | 54.139999 | 51.759998 | 53.830002 | 53.830002 | 2015300 | True | medium_gain |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2015-12-23 | 27.950001 | 28.420000 | 27.440001 | 28.150000 | 28.150000 | 1001000 | True | small_gain |

| 2015-12-24 | 28.270000 | 28.590000 | 27.900000 | 28.400000 | 28.400000 | 587400 | True | small_gain |

| 2015-12-28 | 28.120001 | 28.379999 | 27.770000 | 27.879999 | 27.879999 | 1004500 | False | negative |

| 2015-12-29 | 27.950001 | 28.540001 | 27.740000 | 28.480000 | 28.480000 | 1103900 | True | small_gain |

| 2015-12-30 | 28.580000 | 28.780001 | 28.170000 | 28.250000 | 28.250000 | 1068000 | False | negative |

251 rows × 8 columns

Grouping#

An extremely powerful DataFrame method is groupby().

This is entirely analagous to GROUP BY in SQL.

It will group the rows of a DataFrame by the values in one (or more) columns, and let you iterate through each group.

Here we will look at the average gain among the categories of gains (negative, small, medium and large) we defined above and stored in column gain.

gain_groups = new_df.groupby('gain')

Essentially, gain_groups behaves like a dictionary:

the keys are the unique values found in the

gaincolumn, andthe values are DataFrames that contain only the rows having the corresponding unique values.

for gain, gain_data in gain_groups:

print(gain)

print(gain_data.head())

print('=============================')

large_gain

open high low close adj_close volume \

date

2015-05-07 38.220001 48.73 38.220001 47.009998 47.009998 33831600

profit gain test_column

date

2015-05-07 True large_gain large_gain

=============================

medium_gain

open high low close adj_close volume \

date

2015-01-08 52.590000 54.139999 51.759998 53.830002 53.830002 2015300

2015-01-16 50.180000 51.490002 50.029999 51.389999 51.389999 2183300

2015-01-21 51.200001 53.500000 51.200001 53.410000 53.410000 3248100

2015-02-03 53.830002 55.930000 53.410000 55.779999 55.779999 2885400

2015-02-04 55.529999 57.070000 55.250000 56.740002 56.740002 2498600

profit gain test_column

date

2015-01-08 True medium_gain medium_gain

2015-01-16 True medium_gain medium_gain

2015-01-21 True medium_gain medium_gain

2015-02-03 True medium_gain medium_gain

2015-02-04 True medium_gain medium_gain

=============================

negative

open high low close adj_close volume \

date

2015-01-02 55.459999 55.599998 54.240002 55.150002 55.150002 1664500

2015-01-05 54.540001 54.950001 52.330002 52.529999 52.529999 2023000

2015-01-06 52.549999 53.930000 50.750000 52.439999 52.439999 3762800

2015-01-07 53.320000 53.750000 51.759998 52.209999 52.209999 1548200

2015-01-12 56.000000 56.060001 53.430000 54.020000 54.020000 2407700

profit gain test_column

date

2015-01-02 False negative negative

2015-01-05 False negative negative

2015-01-06 False negative negative

2015-01-07 False negative negative

2015-01-12 False negative negative

=============================

small_gain

open high low close adj_close volume \

date

2015-01-09 55.959999 56.990002 54.720001 56.070000 56.070000 6224200

2015-01-22 53.869999 55.279999 53.119999 54.799999 54.799999 2295400

2015-01-23 54.660000 55.639999 54.299999 55.189999 55.189999 1636400

2015-01-26 55.119999 55.790001 54.830002 55.410000 55.410000 1450300

2015-01-29 52.849998 53.310001 51.410000 52.930000 52.930000 1844100

profit gain test_column

date

2015-01-09 True small_gain small_gain

2015-01-22 True small_gain small_gain

2015-01-23 True small_gain small_gain

2015-01-26 True small_gain small_gain

2015-01-29 True small_gain small_gain

=============================

for gain, gain_data in new_df.groupby("gain"):

print('The average closing value for the {} group is {}'.format(gain,

gain_data.close.mean()))

The average closing value for the large_gain group is 47.0099983215332

The average closing value for the medium_gain group is 39.72307696709266

The average closing value for the negative group is 37.38476184057811

The average closing value for the small_gain group is 36.53367346160266

Other Pandas Classes#

A DataFrame is essentially an annotated 2-D array.

Pandas also has annotated versions of 1-D and 3-D arrays.

A 1-D array in Pandas is called a Series.

A 3-D array in Pandas is created using a MultiIndex.

To use these, read the documentation!

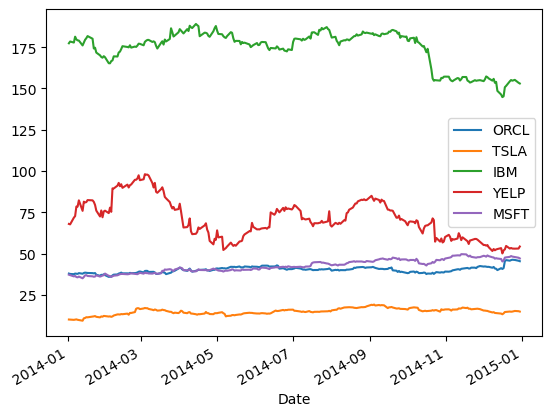

Comparing multiple stocks#

As a last task, we will use the experience we obtained so far – and learn some new things – in order to compare the performance of different stocks we obtained from Yahoo finance.

stocks = ['ORCL', 'TSLA', 'IBM','YELP', 'MSFT']

stock_df = pd.DataFrame()

for s in stocks:

stock_df[s] = pd.DataFrame(yf.download(s,start='2014-01-01',end='2014-12-31', progress = False))['Close']

stock_df.head()

| ORCL | TSLA | IBM | YELP | MSFT | |

|---|---|---|---|---|---|

| Date | |||||

| 2014-01-02 | 37.840000 | 10.006667 | 177.370941 | 67.919998 | 37.160000 |

| 2014-01-03 | 37.619999 | 9.970667 | 178.432129 | 67.660004 | 36.910000 |

| 2014-01-06 | 37.470001 | 9.800000 | 177.820267 | 71.720001 | 36.130001 |

| 2014-01-07 | 37.849998 | 9.957333 | 181.367111 | 72.660004 | 36.410000 |

| 2014-01-08 | 37.720001 | 10.085333 | 179.703629 | 78.419998 | 35.759998 |

stock_df.plot();

Next, we will calculate returns over a period of length \(T,\) defined as:

The returns can be computed with a simple DataFrame method pct_change(). Note that for the first \(T\) timesteps, this value is not defined (of course):

rets = stock_df.pct_change(30)

rets.iloc[25:35]

| ORCL | TSLA | IBM | YELP | MSFT | |

|---|---|---|---|---|---|

| Date | |||||

| 2014-02-07 | NaN | NaN | NaN | NaN | NaN |

| 2014-02-10 | NaN | NaN | NaN | NaN | NaN |

| 2014-02-11 | NaN | NaN | NaN | NaN | NaN |

| 2014-02-12 | NaN | NaN | NaN | NaN | NaN |

| 2014-02-13 | NaN | NaN | NaN | NaN | NaN |

| 2014-02-14 | 0.003700 | 0.320653 | -0.009918 | 0.321849 | 0.012379 |

| 2014-02-18 | 0.009304 | 0.361995 | -0.018485 | 0.355897 | 0.013817 |

| 2014-02-19 | 0.010675 | 0.317279 | -0.016398 | 0.254880 | 0.038195 |

| 2014-02-20 | 0.011096 | 0.405798 | -0.028728 | 0.257501 | 0.036803 |

| 2014-02-21 | 0.010074 | 0.385510 | -0.027558 | 0.170875 | 0.062081 |

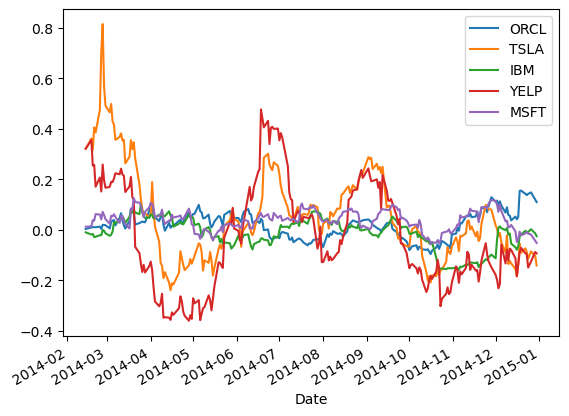

Now we’ll plot the timeseries of the returns of the different stocks.

Notice that the NaN values are gracefully dropped by the plotting function.

rets.plot();

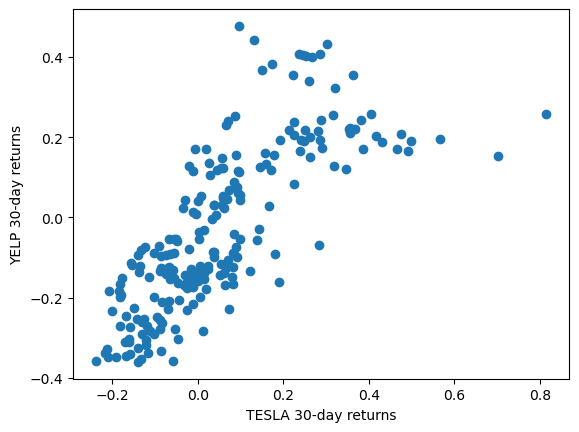

plt.scatter(rets.TSLA, rets.YELP)

plt.xlabel('TESLA 30-day returns')

plt.ylabel('YELP 30-day returns');

There appears to be some (fairly strong) correlation between the movement of TSLA and YELP stocks. Let’s measure this.

The correlation coefficient between variables \(X\) and \(Y\) is defined as follows:

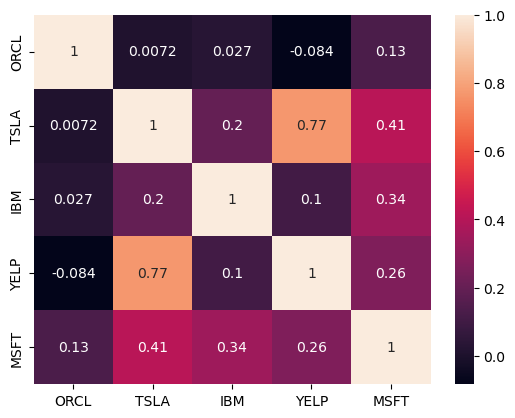

Pandas provides a dataframe method to compute the correlation coefficient of all pairs of columns: corr().

rets.corr()

| ORCL | TSLA | IBM | YELP | MSFT | |

|---|---|---|---|---|---|

| ORCL | 1.000000 | 0.007218 | 0.026666 | -0.083688 | 0.131830 |

| TSLA | 0.007218 | 1.000000 | 0.196371 | 0.769623 | 0.411348 |

| IBM | 0.026666 | 0.196371 | 1.000000 | 0.104705 | 0.343697 |

| YELP | -0.083688 | 0.769623 | 0.104705 | 1.000000 | 0.264703 |

| MSFT | 0.131830 | 0.411348 | 0.343697 | 0.264703 | 1.000000 |

It takes a bit of time to examine that table and draw conclusions.

To speed that process up it helps to visualize the table.

We will learn more about visualization later, but for now this is a simple example.

sns.heatmap(rets.corr(), annot=True);

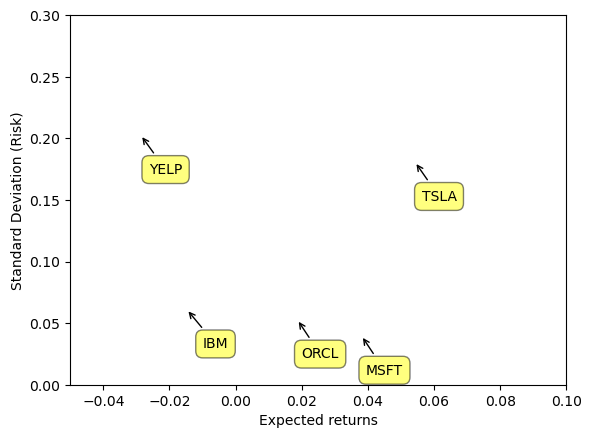

Finally, it is important to know that the plotting performed by Pandas is just a layer on top of matplotlib (i.e., the plt package).

So Panda’s plots can (and often should) be replaced or improved by using additional functions from matplotlib.

For example, suppose we want to know both the returns as well as the standard deviation of the returns of a stock (i.e., its risk).

Here is visualization of the result of such an analysis, and we construct the plot using only functions from matplotlib.

# plt.scatter(rets.mean(), rets.std());

plt.xlabel('Expected returns')

plt.ylabel('Standard Deviation (Risk)')

plt.xlim([-.05,.1])

plt.ylim([0,.3])

for label, x, y in zip(rets.columns, rets.mean(), rets.std()):

plt.annotate(

label,

xy = (x, y), xytext = (30, -30),

textcoords = 'offset points', ha = 'right', va = 'bottom',

bbox = dict(boxstyle = 'round,pad=0.5', fc = 'yellow', alpha = 0.5),

arrowprops = dict(arrowstyle = '->', connectionstyle = 'arc3,rad=0'))

To understand what these functions are doing, (especially the annotate function), you will need to consult the online documentation for matplotlib. Just use Google to find it.